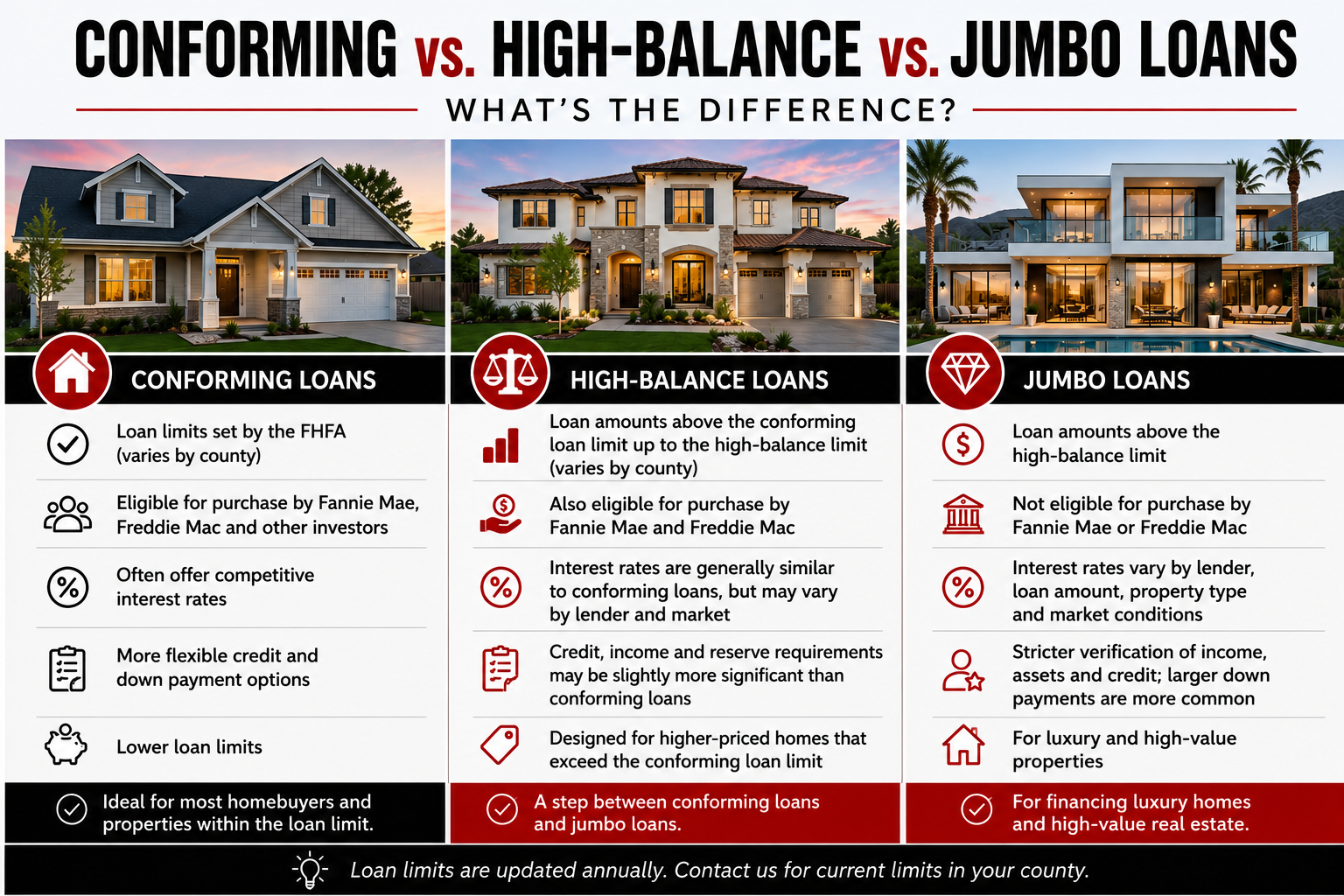

When comparing a conforming vs. jumbo loan, California homebuyers may also encounter a third mortgage…

VA Loan Pest Inspection Requirements in California

One of the most common misconceptions about VA loans in California is that the property must have a completely clear pest inspection report before the loan can close.

That is not always true.

While VA loans in California generally require a pest inspection, borrowers do not always need full Section 1 and Section 2 clearance. In many cases, the lender may only need an NPMA-33 form confirming that the property has no active infestation. Understanding the difference can help veterans, real estate agents, and sellers avoid unnecessary confusion and delays during escrow.

Are Pest Inspections Required on VA Loans in California?

Yes.

For VA home loans in California, lenders require a pest inspection to determine whether the property has an active pest infestation. Most commonly, this refers to termites or other wood-destroying organisms.

The VA requires the property to be free of active pest infestation. However, how that requirement is documented can make a significant difference during the loan process.

What Is the Difference Between a Pest Inspection Report and an NPMA-33?

Many people assume a pest inspection report and an NPMA-33 are the same thing, but they serve different purposes.

A licensed pest control company prepares a full California pest inspection report detailing the property’s condition. It typically identifies all Section 1 and Section 2 findings, including active infestations, dry rot, fungus damage, moisture conditions, earth-to-wood contact, and other items that may require repair or further evaluation.

An NPMA-33, also known as a Wood Destroying Insect Inspection Report, is a standardized form that focuses on whether there is evidence of active infestation or damage from wood-destroying insects or organisms.

For VA loans, the primary concern is whether the property has an active pest infestation. In many cases, an NPMA-33 can provide the documentation needed to confirm the property is free of active infestation without requiring the lender to review the entire pest inspection report.

This distinction is important because once a lender receives the full pest inspection report, it may review all findings listed in the report. If the report identifies Section 1 items, dry rot, or other deficiencies, the lender may require repairs or clearances before closing.

That is why understanding the difference between an NPMA-33 and a full pest inspection report can help veterans, buyers, sellers, and real estate agents better navigate the VA loan process.

Why Some VA Loans Require More Repairs Than Others

Not all lenders interpret pest reports the same way.

Some lenders require:

-

A clear Section 1 report

-

Examples may include:

- Active termites

- Active wood-destroying organisms

- Dry rot

- Fungus damage

- Damaged wood components

-

-

A clear Section 2 report

-

Examples may include:

- Earth-to-wood contact

- Excessive moisture

- Plumbing leaks

- Faulty drainage

- Conditions conducive to future termite activity

-

-

Both Section 1 and Section 2 clearance

These requirements are often lender overlays rather than VA requirements.

At Inner Circle Mortgage, we work with lenders that follow VA guidelines without imposing unnecessary pest inspection overlays whenever possible.

What If the VA Appraiser Notes Dry Rot or Damage?

Even when the lender is relying on an NPMA-33 form rather than a full pest report, the VA appraiser can still identify property condition concerns during the appraisal.

If the appraiser notes issues such as:

- Dry rot

- Damaged wood

- Evidence of termite activity

- Health and safety concerns

- Deferred maintenance

the lender may require additional documentation, repairs, or a clear pest certification before closing.

The lender has the right to request a clear Section 1 clearance and, in some cases, a clear Section 2 clearance based on the appraiser’s findings.

The Bottom Line

The biggest myth is that every VA loan in California requires a completely clear pest inspection report.

The reality is that the property must be free of active pest infestation, but that requirement can often be documented through an NPMA-33 form rather than a full pest report.

Every transaction is different. Appraisal findings, lender requirements, and the property’s condition can all affect the documentation the lender requires.

Working with a lender who understands VA guidelines and California pest inspection practices can help veterans avoid unnecessary delays and keep their transactions moving smoothly.

Questions About VA Loan Requirements?

As a United States Air Force veteran and Broker/Owner of Inner Circle Mortgage, I help veterans and active-duty service members navigate the VA loan process throughout California.

Whether you’re purchasing your first home or using your VA benefits again, I’m happy to answer your questions.

For additional information about VA minimum property requirements, visit the U.S. Department of Veterans Affairs home loan guidance.

Learn More About VA Loans in Folsom and Throughout California

Related Posts